月とスッポンさんのブログ

ブログ

アナリストはリセッション開始以来もっとも強気らしい^^;

月とスッポンさん

投稿:2009/10/10 20:34

更新:2009/10/10 23:48

Analysts at Most Bullish Level in Two Years

From the start of the recession in December 2007 through mid-2009, analysts consistently found themselves lowering forecasts for the companies they cover. Whether it was a factor of the weak economy or in reaction to poor earnings and guidance, estimates that previously looked good to the analysts started to look too high.

Each week in our Earnings Estimate Revisions report we calculate the net percentage of companies in the S&P 1500 that have seen their earnings estimates raised over the last four weeks. Since we began publishing the report in January 2009 and until recently, the net revisions ratio was constantly negative. This indicated that the percentage of companies seeing their earnings estimates lowered exceeded the number of companies whose estimates were raised. Given that the market tends to price in investors' expectations of the future, earnings results and an economy that failed to live up to expectations led to lower prices, and vice versa. Beginning this Spring, however, we began to see our Earnings Revision Ratio turn higher, and by Summer it actually moved into positive territory. No longer were analysts scrambling to cut numbers, but instead they were finding that their previous estimates were too low.

This brings us today, and the start of Q3 earnings season. As shown below, analysts are more bullish heading into the current earnings season than they have been at the start of any other earnings season since the recession began. Over the last four weeks, analysts have raised forecasts for 638 companies in the S&P 500 and lowered forecasts for 391. This works out to a net of 247, or 16.45% of the index. While some would argue that bullish analysts are a contrarian signal, we would note that earnings revisions were negative for several quarters and turned much more negative before they became a contrarian signal. With that said, the positive earnings revision ratio does set the bar higher than in prior quarters. Beginning today, we'll find out of the bar is too high.

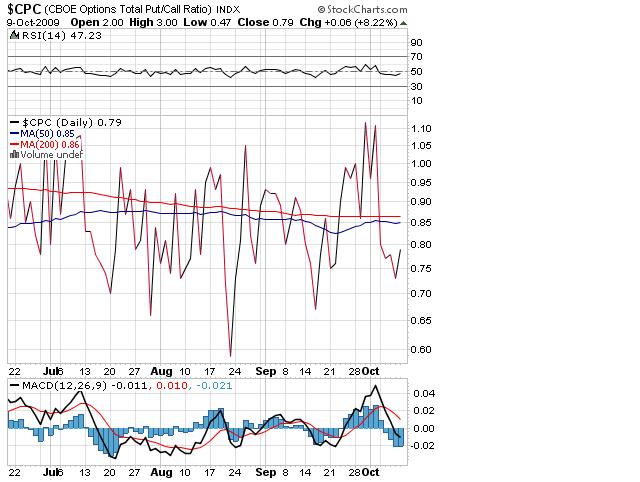

画像2は昨日のダウプットコールレシオです。

プットが買われだした???

逆に怖いです。

同じく、これは逆指標だと思うので、そろそろ注意かな~と思います。

マインド指数はどれをとっても総楽観に近い、、、

プットコールレシオはプットが買われだしたので警戒心はあるようですが、、、